September was a busy month for team Crux, with packed agendas and incredible conversations at RE+ and NYC’s Climate Week (including a great event with Nasdaq). We also hosted our quarterly in-person offsite meeting, where we built out our Q4 product roadmap to best meet the needs of those financing the clean energy transition.

Our October market update summarizes key themes that have been coming up in conversations — and what’s changed since our last update just a couple of months ago.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

Market pricing is drifting up, with spot PTCs transacting in the low-to-mid 90s (before insurance and fees), though this represents a premium over the pricing for ITC credits, which continue to gross in the low-90s for utility scale and well-structured community solar and C&I portfolios (lower for residential roof portfolios and smaller credits). Credit pricing continues to be stratified according to the portfolio size and perceived risk premium (tied primarily to tax credit type and security package), with further adjustments within the bands to reflect fiscal year timing, project/developer-specific traits, and unique payment terms, as illustrated in Figure 1. Virtually all deals carry some form of insurance, including PTC deals, which knocks 2-3 points off of the net pricing that developers realize.

We encourage credit buyers with good visibility into their future years’ tax liabilities to look seriously at 2024 and 2025 tax credit deals for several reasons. First, we see 2023 credits transacting at a premium due to the relatively high near term demand. As we approach year end, the market is likely to become even tighter, effectively deepening the slope of the credit price curve and boosting the relative appeal of 2024 and 2025 credits.

Additionally, buyers generally pay nothing for a deal until it is transacted, but providing developers some cash flow certainty better enables them to access capital and obtain equipment necessary to complete their projects. Access to capital is and remains a fundamental requirement for energy transition companies to thrive.

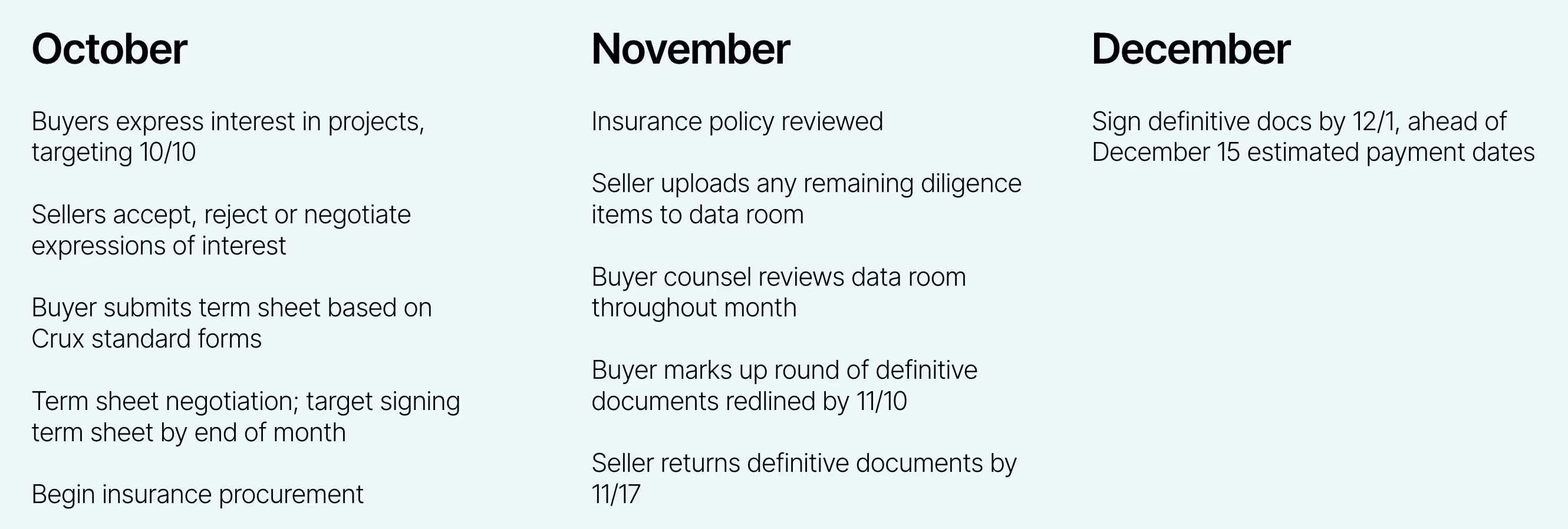

Buyers who are not yet active in the market for 2023 credits may be challenged to find credits to purchase before year end. In order to close a deal this year, buyers and sellers must be prepared to move through key transaction milestones at a relatively efficient pace (outlined in Figure 2), including expressing interest, negotiating a term sheet and definitive documents, and completing diligence by early December. For an even better sense of the milestones and complexities that parties must navigate in a transferable credit deal, check out our team’s recent webinar, featuring perspectives from Kirkland & Ellis, Invenergy, and insurer Aon.

As January 2024 brings in the new tax year, we generally expect the demand side of the market to relax and we may see deals done at relatively lower prices at that point (or, in return for higher prices, staggered or delayed payment terms to hold buyers NPV-neutral). Developers looking to obtain the best possible pricing need to set themselves up to run a competitive price discovery market. Crux is well positioned to support this process — sellers have nothing to lose and everything to gain from listing credits for sale on the platform as soon as practicable (find out more about that process here).

Amidst this tightening market, buyers are warming quickly to one of the more unique benefits of the transferability structure: the ability to build portfolios of tax credits across multiple projects in order to meet average price and total credit value targets. As we suggested in our last state of the market report, standardization of terms and documents becomes essential in this portfolio approach; it simply is not realistic for either buyers or sellers to negotiate individual terms for multiple deals at once.

In June, the market reacted positively to regulatory guidance from the US Treasury Department and from the OECD, but many different regulatory factors are relevant to this new market, and guidance from the US banking regulators on implementing Basel III Endgame requirements (which apply to the largest banks) have expected chilling effects on the tax equity market.

In brief, the regulators' proposed guidance assigns a higher risk-weighting to active investment in private entities, which would include virtually all tax equity (TE) partnership structures. With that higher risk-weighting, large banks investing via tax equity structures would then be required to meet higher capital requirements, which would be expected to limit appetite.

TE will continue to play an essential role in clean energy project finance for many years to come, in no small part because the partnership structure allows developers to monetize depreciation and the sale of the project to a partnership provides an opportunity to adjust the cost basis of the project — leading to higher values of tax attributes. A desirable financing structure, particularly for large projects, leverages TE to provide initial capital, and enables the TE partner to syndicate, or sell, transferable tax credits (TTCs) once the financed project enters service. Basel III endgame guidance would reduce the attractiveness of this structure for the largest banks, and risks limiting interest in TE among some large bank sponsors. The rules are not yet final and market participants have been submitting comment letters communicating the perceived negative impacts to the regulators.

_________________________________

The market is full steam ahead on transferability. Crux has hundreds of millions of dollars worth of TTCs in process. We maintain wide channels of distribution through our platform, including with the largest intermediaries in the market. We encourage developers to reach out to us today to gain access to this marketplace and to get competitive pricing for their credits.