Updated July 3, 2025

After months of debate and negotiation — and overnight voting sessions in both chambers — Congress passed President Donald Trump’s signature tax and spending legislation, delivering it to the President’s desk by his stated July 4 deadline.

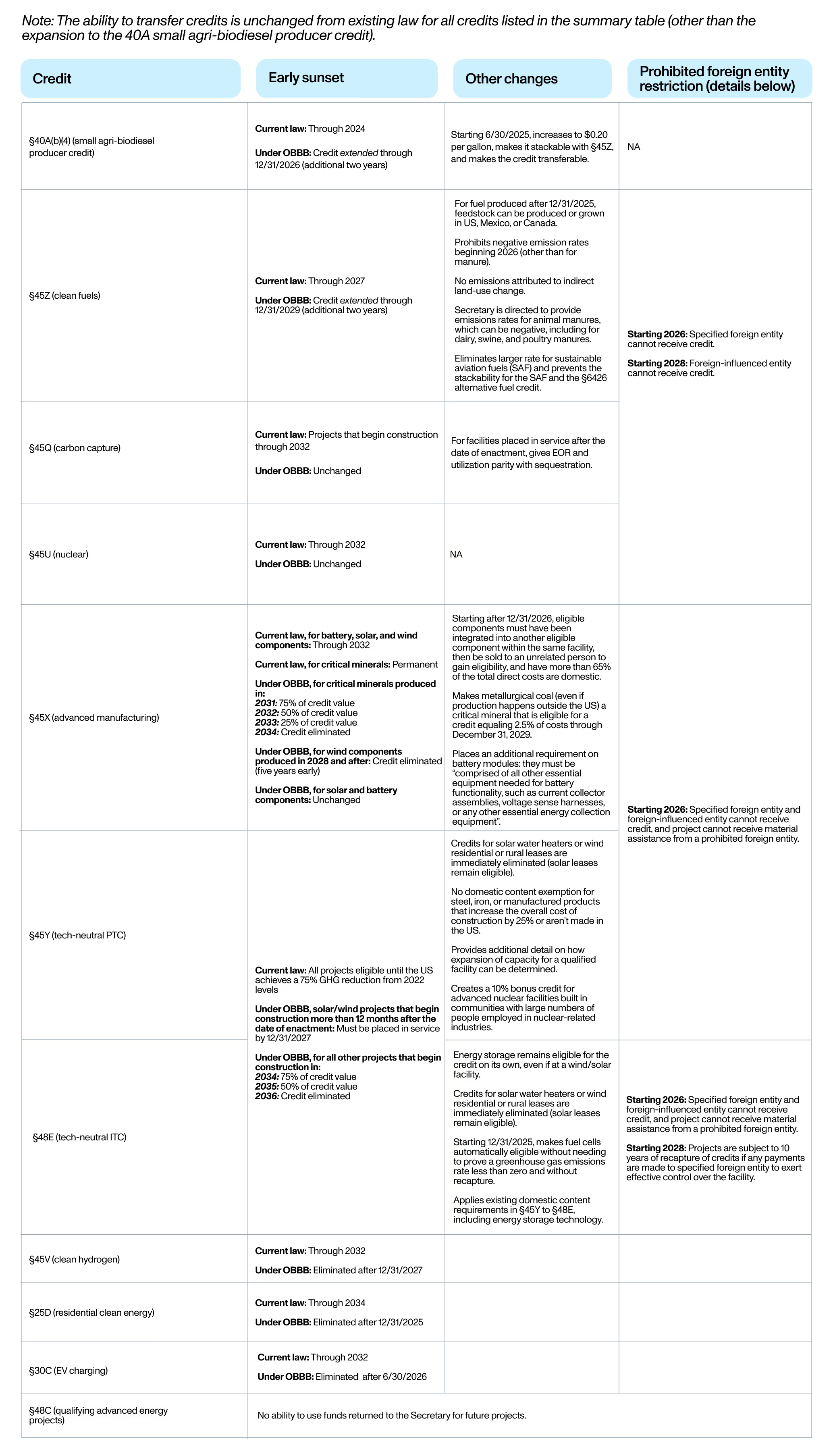

While many of the proposed cuts to energy and manufacturing tax credit provisions were moderated compared to the May House version, the One Big Beautiful Bill (OBBB) Act ultimately adopted a punitive stance toward solar and wind technologies. In contrast, credits for other sectors were largely preserved or, in some cases, expanded.

An intermediate version of the bill released June 27th introduced even more restrictive measures than those found in the original House text. These included a new excise tax on all wind and solar facilities that fail to meet stringent Foreign Entity of Concern (FEOC) requirements, as well as a reversion to a strict “placed-in-service” requirement for qualification — replacing the more flexible, longstanding “commence construction” standard.

Moderate senators, most notably Lisa Murkowski (R-AK), John Curtis (R-UT), and Thom Tillis (R-NC), led efforts to soften the bill’s treatment of solar and wind. Their push resulted in several key revisions in the final version, including a one-year “commence construction” carveout, full credit eligibility for projects placed in service by the end of 2027, and the reinstatement of residential solar eligibility under the tech-neutral credit regime.

The final language maintained the original Senate treatment of transferability, and even expanded it to the §40A small agri-biodiesel producer credit. All applicable credits retain transferability for the full life of the reformed credits. However, tax credit buyers will now be subject to FEOC requirements.

Wind and solar projects that begin construction within 12 months of the date of enactment of the law retain the ability to use the “commence construction” date to earn the technology-neutral credits under §48E and §45Y. However, after that year, a project must be placed in service by the end of 2027 to be eligible for the credit.

As noted, residential solar retained eligibility for §48E and §45Y, reversing the previous House elimination. Additionally, the final Senate text restored five-year accelerated depreciation eligibility for solar and wind projects that otherwise qualify for §48E and §45Y requirements.

The final bill largely retains the FEOC structure proposed by the House and tweaked by the Senate Finance Committee. Changes in the final language included:

Find the latest FEOC definitions and changes in our FEOC cheat sheet.

Please note, this is a fluid situation and any analysis is subject to change. We will continue to monitor developments and provide timely updates as the legislative process unfolds.